How Do I Get Money Back From a Scammer?

Author: Shaun Packiarajah

Disclaimer: This article was originally published in 2018 and has been updated in October 2025 to reflect more current information, resources, and advice. Scams and recovery options continue to evolve, so always double-check with your bank, payment provider, or local consumer protection authority for the latest guidance.

So the worst has come to pass - you realise you parted with your money too fast, and the site you used was a scam - what now? Well first of all, don’t despair!!

If you think you have been scammed, the first port of call when having an issue is to simply ask for a refund. This is the first and easiest step to determine whether you are dealing with a genuine company or scammers. Sadly, getting your money back from a scammer is not as simple as just asking.

If you are indeed dealing with scammers, the procedure (and chance) of getting your money back varies depending on the payment method you used.

- PayPal

- Debit card/Credit card

- Bank transfer

- Wire transfer

- Google Pay

- Bitcoin

PayPal

Good news: PayPal gives you strong protection. You can file a dispute within 180 days of your purchase.

You can get a refund if:

- Your order never arrives, and the seller cannot provide proof of delivery.

- The scammer sends you something completely different (e.g., a controller instead of a PlayStation).

- The product condition was misrepresented (sold as new but arrives used).

- The item is missing undisclosed parts.

- The item is counterfeit.

Start your claim directly through PayPal’s Resolution Center.

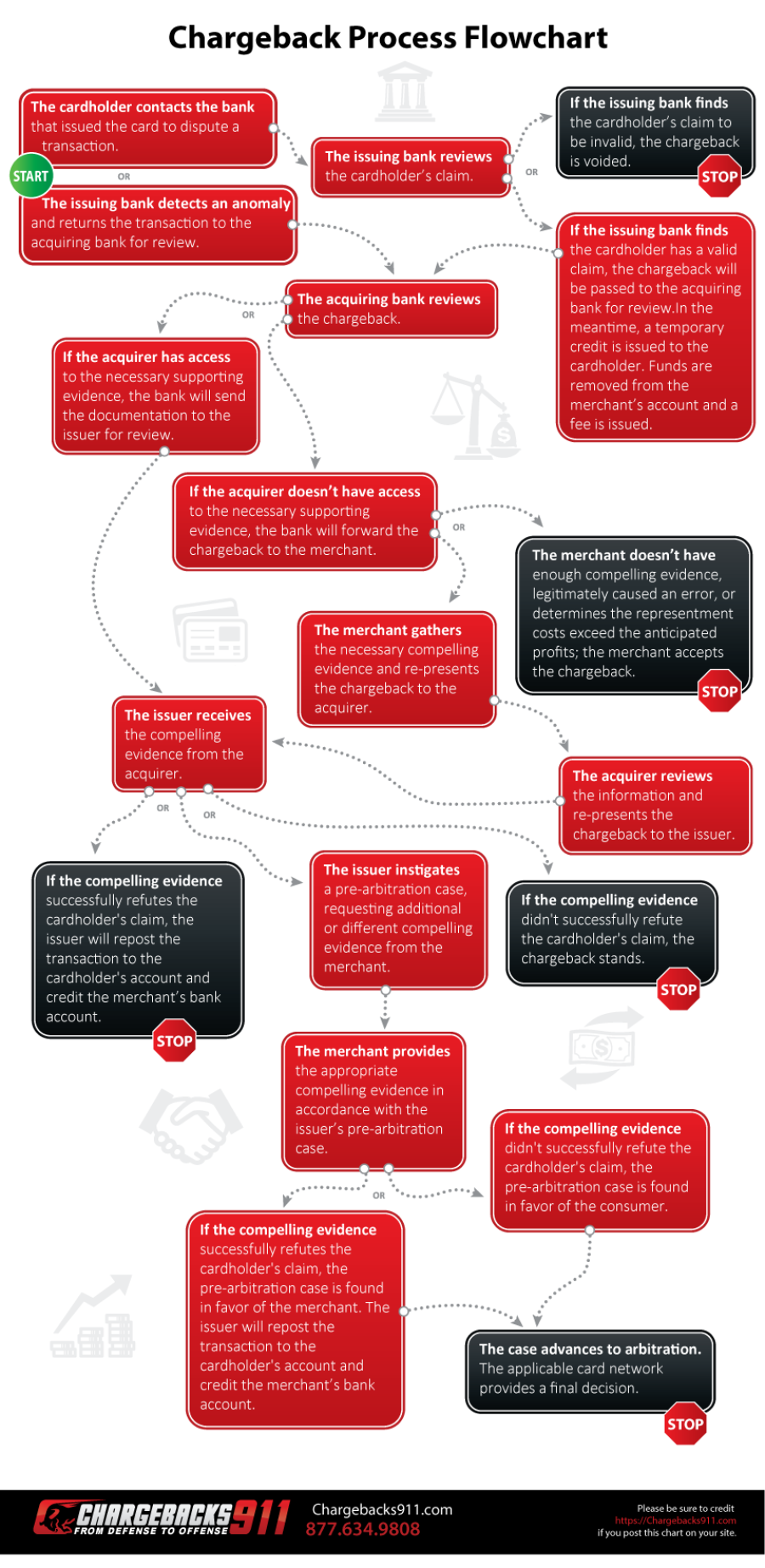

Credit Card or Debit Card

Paying by card is usually your safest bet when it comes to online scams, thanks to chargeback and, in the UK, Section 75. With chargeback, your bank can pull money back from the merchant’s bank if you didn’t get what you paid for, the item never arrived, or the company went bust. You generally have 120 days to make a claim, so act quickly and keep all receipts, emails, and order confirmations as evidence.

You can use a chargeback when:

- Goods or services are faulty, never arrive, or aren’t as described

- A company goes bankrupt after you’ve already paid

- You’ve been charged twice or for the wrong amount

- You spot a fraudulent or unauthorised transaction

If you’re in the UK, Section 75 of the Consumer Credit Act adds another layer of protection for purchases between £100–£30,000. Unlike chargeback, it’s a legal guarantee—your card provider is just as responsible as the seller if things go wrong. The only catch: avoid paying via a third-party like PayPal with your card, as this can invalidate Section 75 rights. Wherever you are, credit cards remain one of the best tools for fighting back against scammers.

Note: Be careful not to use a third-party such as PayPal when paying by credit card. This can invalidate your right to claim under Section 75. For further details look here.

Bank Transfer

If you’ve sent money via bank transfer to a scammer, time is critical. Contact your bank immediately and explain the situation—they may be able to recall the funds before they are withdrawn. If the recovery attempt fails, you can escalate by filing a formal complaint with your bank or contacting your local financial ombudsman. According to Wise, as long as you can recognize scammers and share the correct recipient details, your money should reach its destination without issues.

Wire Transfer Services

Be extremely cautious with services like MoneyGram, PayPoint, or Western Union. Scammers often prefer these because once the cash is collected, it’s nearly impossible to trace or recover.

Unauthorised Mystery Payments

Noticed a strange charge on your bank or card statement? It could be an unauthorised withdrawal. Contact your bank immediately to report it. Depending on where you live, financial regulations may entitle you to a refund for fraudulent or unauthorised transactions. In the UK, banks are required to refund most victims under the Payment Services Regulations 2017.

Google Pay

If you suspect someone used your Google Pay account without permission, Google has a built-in dispute system where you can report, cancel, or challenge suspicious payments. Check your transaction history, act quickly, and provide as much detail as possible when raising your claim.

Bitcoin and Other Cryptocurrencies

Unfortunately, cryptocurrency transactions are almost always irreversible. Once coins leave your wallet, recovering them is extremely unlikely. You can try contacting the exchange or platform you used, but refunds are rare.

Beware of so-called “crypto recovery experts” or “agents” who promise to get your money back for a fee—these are usually scams themselves. For more insight, read our article: Can Cryptocurrency Be Recovered From Scammers?

For more detailed instructions, see: How to Get Your Money Back From a Scam

To learn how to stay safer, read: What Are Safe Ways To Pay Online?

Frequently Asked Questions

1. How quickly should I act after being scammed?

Immediately. The sooner you contact your bank, payment provider, or platform, the higher your chances of recovering money. Delays often mean funds are gone for good.

2. Can I always get my money back through a chargeback?

Not always. Chargeback depends on your bank’s investigation and the evidence you provide. Keeping emails, receipts, and transaction IDs greatly improves your chances.

3. What if I used cryptocurrency?

Crypto is the hardest to recover. Once it’s gone, it’s usually gone forever. Reporting to your local cybercrime unit is still important, but avoid anyone who claims they can guarantee recovery.

4. Should I report scams to the police?

Yes. Even if you don’t get your money back, filing a police report creates a record, may support your bank complaint, and helps authorities track wider scam networks.

5. Is it safe to use wire transfers for strangers online?

No. Wire transfers are nearly impossible to reverse. If you don’t personally know the recipient, avoid using them for online transactions.

Report a Scam!

Have you fallen for a hoax, bought a fake product? Report the site and warn others!

Scam Categories

Help & Info

Top Safety Picks

Your Go-To Tools for Online Safety

- ScamAdviser App - iOS : Your personal scam detector, on the go! Check website safety, report scams, and get instant alerts. Available on iOS

- ScamAdviser App - Android : Your personal scam detector, on the go! Check website safety, report scams, and get instant alerts. Available on Android.

- NordVPN : NordVPN keeps your connection private and secure whether you are at home, traveling, or streaming from another country. It protects your data, blocks unwanted ads and trackers, and helps you access your paid subscriptions anywhere. Try it Today!

Popular Stories

As the influence of the internet rises, so does the prevalence of online scams. There are fraudsters making all kinds of claims to trap victims online - from fake investment opportunities to online stores - and the internet allows them to operate from any part of the world with anonymity. The ability to spot online scams is an important skill to have as the virtual world is increasingly becoming a part of every facet of our lives. The below tips will help you identify the signs which can indicate that a website could be a scam. Common Sense: Too Good To Be True When looking for goods online, a great deal can be very enticing. A Gucci bag or a new iPhone for half the price? Who wouldn’t want to grab such a deal? Scammers know this too and try to take advantage of the fact. If an online deal looks too good to be true, think twice and double-check things. The easiest way to do this is to simply check out the same product at competing websites (that you trust). If the difference in prices is huge, it might be better to double-check the rest of the website. Check Out the Social Media Links Social media is a core part of ecommerce businesses these days and consumers often expect online shops to have a social media presence. Scammers know this and often insert logos of social media sites on their websites. Scratching beneath the surface often reveals this fu

Disclaimer: This article was originally published in 2018 and has been updated in October 2025 to reflect more current information, resources, and advice. Scams and recovery options continue to evolve, so always double-check with your bank, payment provider, or local consumer protection authority for the latest guidance. So the worst has come to pass - you realise you parted with your money too fast, and the site you used was a scam - what now? Well first of all, don’t despair!! If you think you have been scammed, the first port of call when having an issue is to simply ask for a refund. This is the first and easiest step to determine whether you are dealing with a genuine company or scammers. Sadly, getting your money back from a scammer is not as simple as just asking. If you are indeed dealing with scammers, the procedure (and chance) of getting your money back varies depending on the payment method you used. PayPal Debit card/Credit card Bank transfer Wire transfer Google Pay Bitcoin PayPal Good news: PayPal gives you strong protection. You can file a dispute within 180 days of your purchase. You can get a refund if: Your order never arrives, and the seller cannot provide proof of delivery. The scammer sends you something completely different (e.g., a controller instead of a PlayStation). The product condition was misrepresented (sold as new but arrives used). The item is missing undisclosed parts. The item is counterfeit. Start your claim directly through Pay